Why Textbook Kelly Criterion Fails in Live Trading (And How Maya Fixes It)

Position Sizing, Kelly Criterion, and Markets

Why "textbook" Kelly fails in live trading, and how market-aware filters solve the correlation problem

Position Sizing: What Sports Bettors Know That Most Traders Don't

Walk into any serious sports betting operation and ask what separates the people who beat the books from the people who eventually go broke. They won't say handicapping. They won't say feel for the game. They'll say the same thing, every time.

Position sizing.

How much to put on each bet, given your edge, your bankroll, and the odds you're being offered. Get that wrong and it genuinely doesn't matter how sharp your picks are. A sports bettor with a real 55% edge can still zero out an account in a month by betting flat 10% on every game. The math of ruin doesn't care how good the analysis is.

The same is true in trading, and almost nobody talks about it. Everyone wants to argue about entries (what indicator to use, what setup to trade, whether to buy the dip or wait for confirmation). Meanwhile the single biggest determinant of whether you keep your money over a 5-year horizon gets about 2% of the conversation.

The Kelly Criterion, and Why Sharp Bettors Worship It

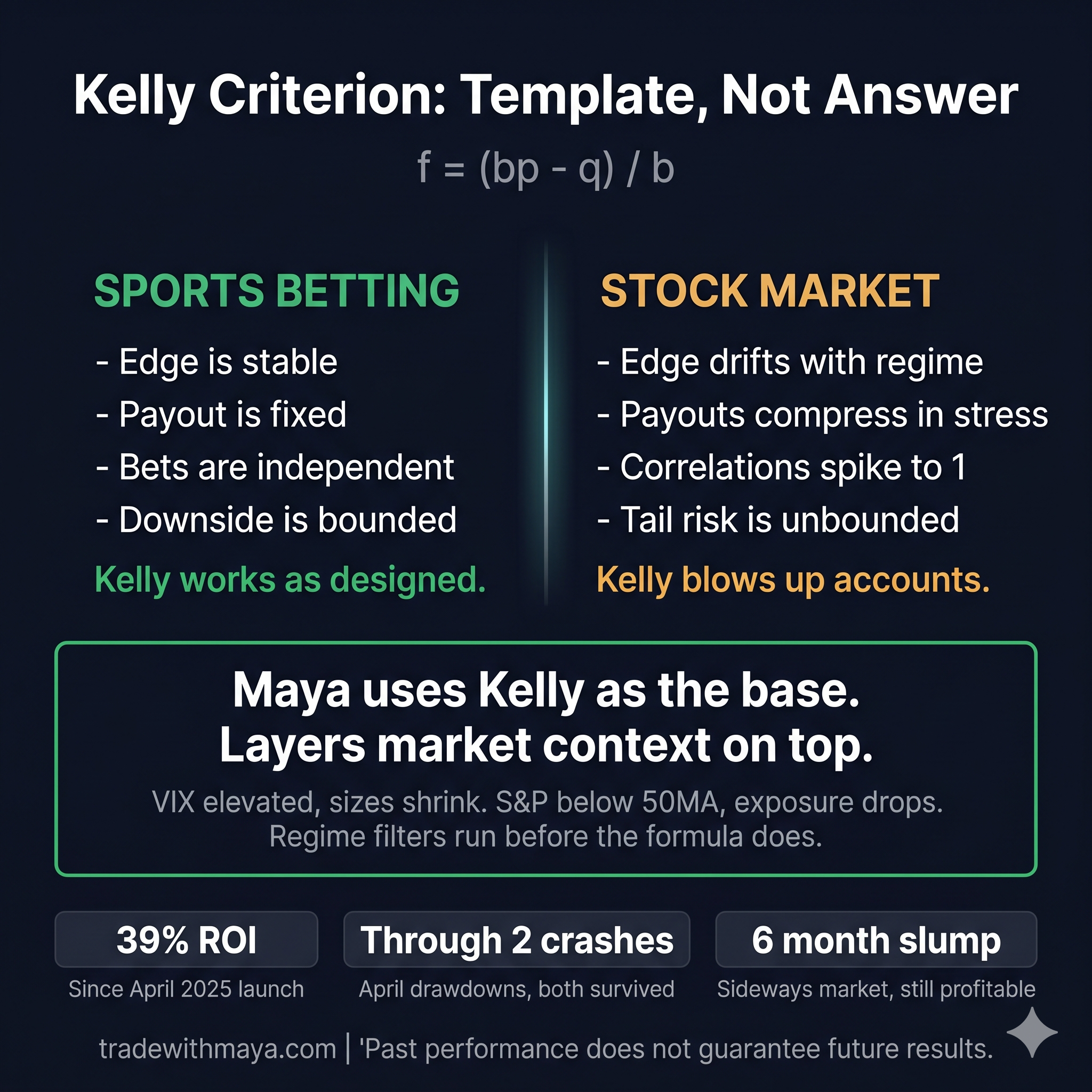

In 1956 a Bell Labs researcher named John Kelly published a paper on optimal bet sizing. The formula was simple and mathematically airtight for any repeated wager where you have a known edge and known odds.

Where f is the fraction of your bankroll to bet, p is your probability of winning, q is your probability of losing, and b is the payout ratio. The idea: bet more when you have a bigger edge, bet less when the edge shrinks, and never bet an amount that risks permanent damage to the bankroll. The formula maximizes long-run compound growth, and seventy years after it was published, nobody has come up with a better starting point.

Ed Thorp used Kelly to beat blackjack in Las Vegas and then ran a hedge fund on the same principles. Bill Gross cited it as foundational to how he sized positions at PIMCO. Every serious card counter, poker pro, and sports book arbitrage team uses some version of it.

Why Kelly Works in Sports Betting

Kelly is built around a specific set of assumptions, and being honest about what they are matters.

The formula assumes your edge is a known, stable number, the payout is fixed before the bet is placed, each bet is independent from the last, and your maximum downside is bounded at whatever you wagered. In sports betting, every one of those holds reasonably well. The game starts, it ends, you win or lose, and the environment doesn't suddenly turn hostile between tipoff and the final whistle.

Now try to port that same formula directly onto the stock market.

Why Kelly Fails in the Markets

Full Kelly applied naively to trading has blown up more accounts than any single strategy in history. The reason is simple: Kelly is not market aware.

Your edge on any given trade is not a stable number. A breakout strategy with a 55% win rate in a trending market might run at 35% in a choppy one. A premium selling strategy that thrives when volatility is elevated runs dry the moment VIX compresses and there's nothing worth collecting. The payout ratio shifts with it, and the same trade structure that pays 1.8 to 1 in a high-vol environment might pay 0.6 to 1 when spreads collapse. None of that shows up in the formula. Kelly just keeps telling you to bet the same fraction because the inputs you fed it last month haven't been updated.

The correlation problem makes it worse. Kelly assumes your bets are independent. Your stock positions are not. In a market crash, everything correlates to 1, and the five Kelly-sized positions you thought were diversified turn out to be one giant bet on "things don't fall apart today." And when they do fall apart, a trader using leverage or short volatility can lose far more than what Kelly's math assumes, because the formula treats your downside as bounded at the wager amount. In markets, without defined risk, it often isn't.

Professional traders almost never use full Kelly for this reason. They use half Kelly, quarter Kelly, or something homegrown that caps position size well below what the raw formula suggests. The formula is the starting point. What you layer on top of it is the actual work.

What a Market-Aware Version Actually Looks Like

Maya uses a hybrid Kelly. The base formula is still there, sizing up when the edge is strong and pulling back when it isn't. But layered on top are regime filters that the original formula has no concept of.

When VIX is elevated, position sizes shrink regardless of what Kelly says about recent performance. When the S&P 500 is below its 50-day moving average, overall exposure drops. During extended slumps where nothing is working, Maya opens fewer positions and keeps each one smaller than the formula alone would suggest, because the formula doesn't know the regime has shifted.

The same trade setup gets a meaningfully different position size in March than it does in October, because the market those trades are living inside is not the same market. When conditions are hostile, the system pulls back. When they're supportive, it leans in. That second part is what most retail traders never build.

The Results

Maya launched in April 2025 and has returned 39% on the portfolio in the 12 months since. That window included two sharp drawdowns (both in April) and a six-month stretch where the indices went essentially sideways. A pure Kelly model, blind to market context, would have taken full hits in both crashes and kept pushing bets through the dead zone.

Maya didn't, because the sizing was already contracting before the drawdowns played out. Smaller positions going in, faster exits coming out, nothing heroic during the chop.

39% in a year that included two crashes and six months of nothing is not a function of picking better stocks. It is a function of knowing how much to risk and when.

The Lesson

Kelly is a masterpiece of a formula and every serious trader should understand it. But sending it straight out of the textbook into a live account is how smart people lose money slowly and then all at once. The formula was built for a world where edges are stable, payouts are fixed, and outcomes are independent. Markets are none of those things for any sustained stretch, and the formula has no mechanism to notice when that's changed.

If your position sizing doesn't respond to regime shifts, you're running 1956 math against a 2026 market, and the market has no obligation to cooperate.

Use Kelly as the foundation. What you build on top of it is where the real work happens.

Maya AutoTrading is built on exactly this approach: rules-based position sizing that reads the market instead of ignoring it. 39% since launch through two crashes and a half year of nothing. The full track record is public before you spend a dollar.

Ready to Trade Like a Professional

Stop guessing at position size. Let Maya's hybrid Kelly algorithm read the market and adapt automatically.

View Live Track RecordShare this post

Comments 0

Leave a Comment

No comments yet. Be the first to comment!

Stay Updated

Subscribe to our newsletter for the latest trading insights and updates.

Autotrading is Live

Maya sends the signals. PeakBot submits the orders to your brokerage. You never lift a finger.

See How It Works